- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Geothermal Drill Bits Market: Current Analysis and Forecast (2025-2033)

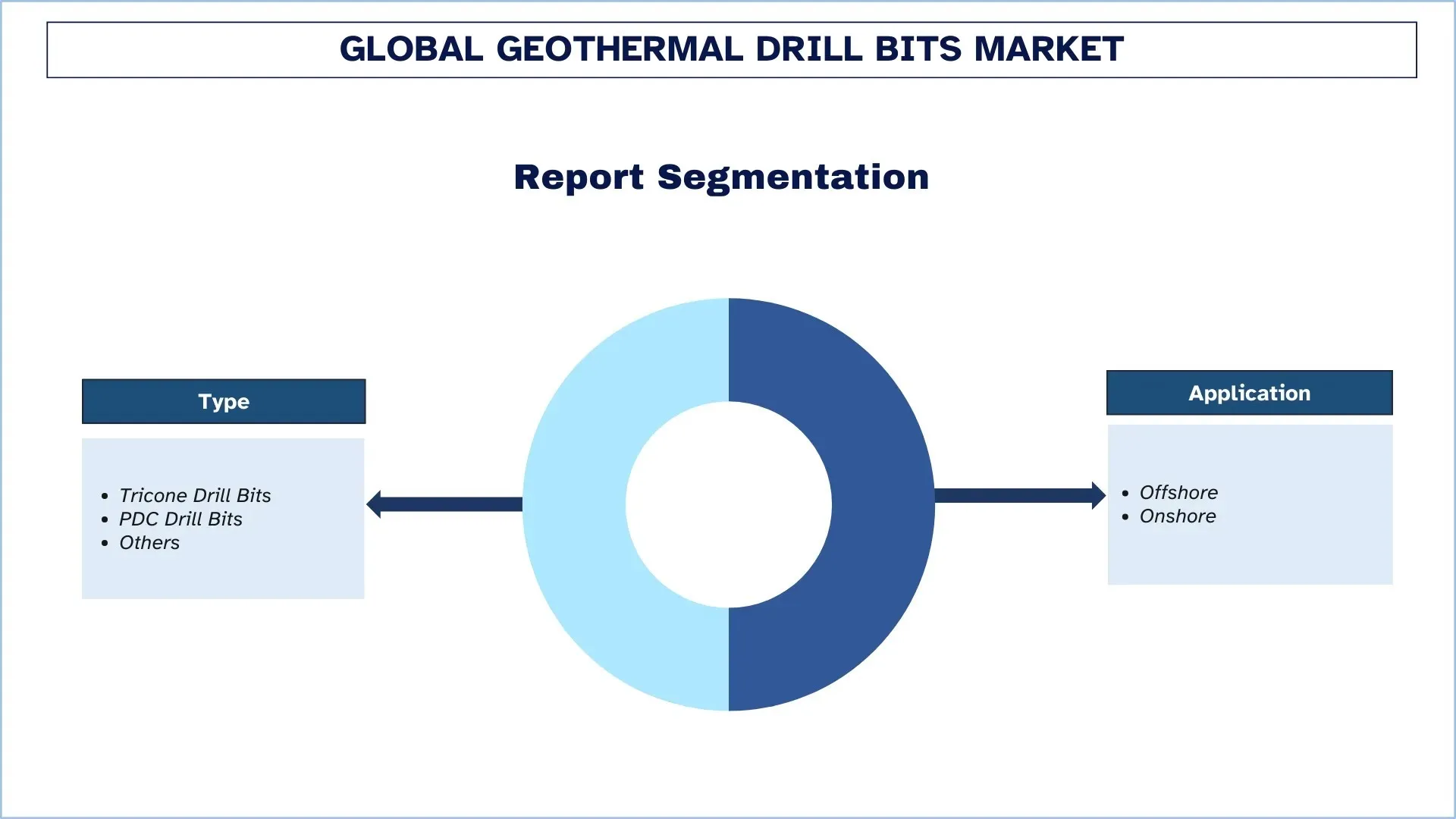

Emphasis on Type (Tricone Drill Bits, PDC Drill Bits, and Others); Application (Offshore and Onshore); and Region/Country

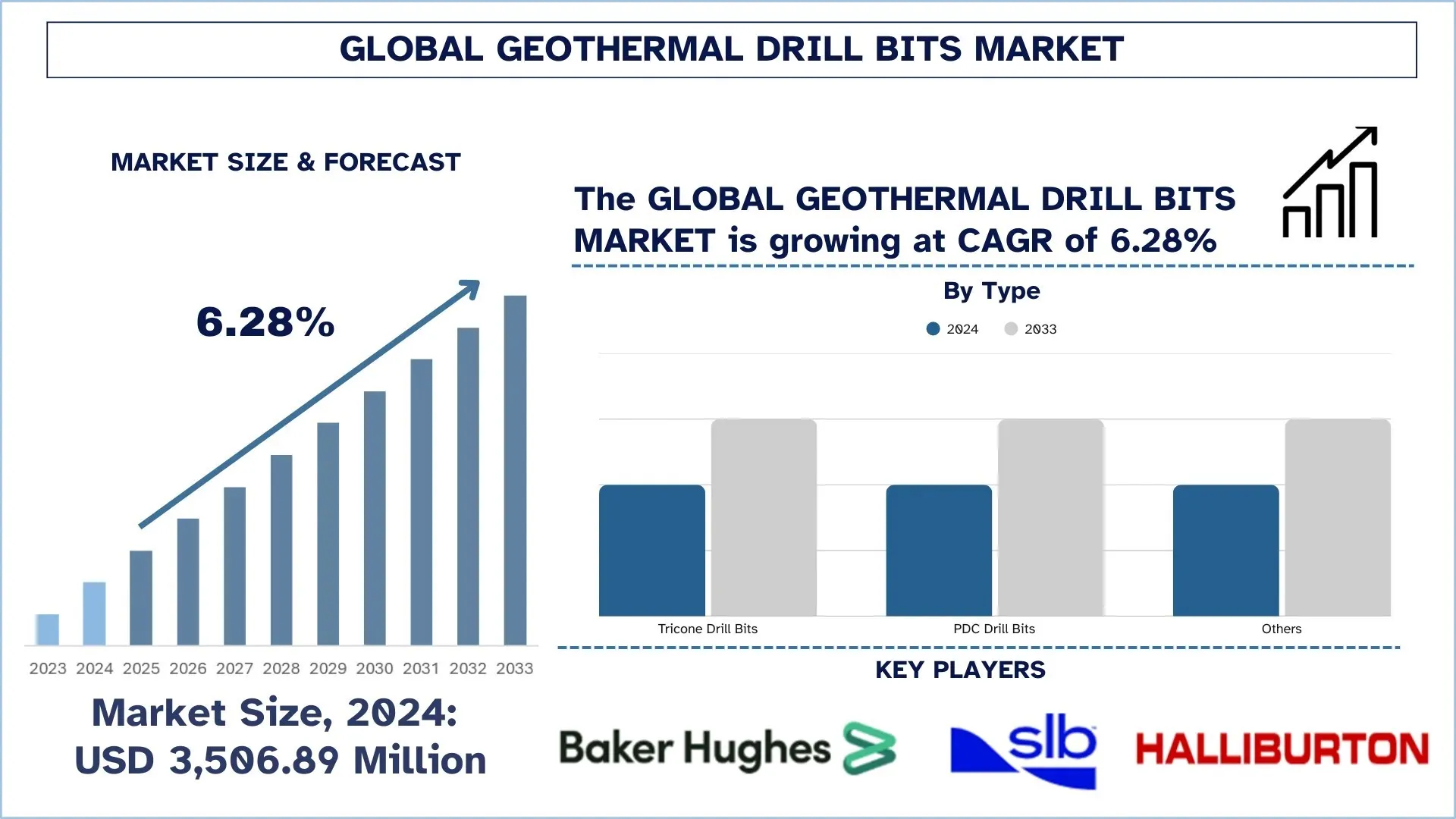

Global Geothermal Drill Bits Market Size & Forecast

The Global Geothermal Drill Bits Market was valued at USD 3,506.89 million in 2024 and is expected to grow at a CAGR of around 6.28% during the forecast period (2025–2033F), driven by expanding geothermal power and direct-use heat deployments, rising drilling activity for deeper, higher-temperature reservoirs, and the need to reduce well construction costs and nonproductive time in hard, abrasive formations, where conventional drilling performance is constrained.

Geothermal Drill Bits Market Analysis

The growing use of geothermal drill bits is gaining more and more importance due to a push to increase the size of firm, low-carbon geothermal power and direct-use heat, which is accelerating the demand to find methods of drilling deep geothermal wells that can endure high temperatures, hard and abrasive geological structures, and harsh downhole conditions, as well as increase penetration rates and reduce cost-per-meter. Geothermal drill bits are regarded as a critical enabling technology to next-generation geothermal development, as it has a direct impact on the time spent drilling, the frequency of trips, the quality of the wellbores and the economics of the project itself, and it is a necessity in exploration, production, injection and make-up wells of utility-scale power systems, district heating networks, and industrial heat supplies. This is further reinforced by increased interest in additional resources, higher-enthalpy resources, and engineered geothermal systems (such as EGS), which drive demand for thermal stability, bearing and seal integrity, impact resistance, and vibration control. Additionally, market growth requires sustained breakthroughs in materials and bit design, including thermally stable cutter technology, enhanced tungsten carbide and hard-facing technology, high-temperature alloys and seal packages, and more reliable, predictable end-to-end performance in geothermal environments through superior drilling analytics and feedback design loops.

Global Geothermal Drill Bits Market Trends

This section discusses the key market trends that are influencing the various segments of the global geothermal drill bits market, as found by our team of research experts.

Rising Adoption of PDC and Hybrid Bits

The growing adoption of PDC and hybrid drill bits is one of the major trends in the global geothermal drill bits market, as providers focus more on the rate of penetration (ROP), longer bit runs, and minimized trips in abrasive, hard geothermal reservoirs. PDC bits are replacing share as their shearing cutting action can provide faster drilling and better footage within appropriate operating periods, and newer cutter materials and thermal-management designs are increasing their operating window in high-temperature geothermal settings. Simultaneously, hybrid bits (combining PDC cutting elements with roller-cone designs) are being utilized to enhance stability and minimize drilling dysfunction, particularly at intervals where impact loading, interbedded hardness, and vibration may limit conventional PDC performance. This conversion is supported by field data indicating that current versions of PDC solutions can be more efficient than traditional roller-cone performance in hard crystalline rock and enhance both ROP and bit life in geothermal-like drilling operations. For example, Baker Hughes is promoting its Vulcanix geothermal Kymera hybrid bit on the premise that it is meant to be used in a deeper and longer drill in a hotter environment and the hybrid architecture is an instance of a reliability and consistency lever in geothermal wells; the company even published a geothermal case study in Utah on the use of its Vulcanix PDC solution to do better in hard-rock drill. Therefore, the market is trending toward increased adoption of PDC and hybrid bits as geothermal developers aim to achieve quantifiable cost-per-meter savings by accelerating drilling, minimizing failures resulting from vibrations, and extending production life in high-temperature, hard-rock environments.

Geothermal Drill Bits Industry Segmentation

This section provides an analysis of the key trends in each segment of the global geothermal drill bits market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Tricone Drill Bits Segment held the Largest Market Share in the Geothermal Drill Bits Market.

Based on type, the global geothermal drill bits market is segmented into Tricone Drill Bits, PDC Drill Bits, and Others. In 2024, the Tricone Drill Bits segment is anticipated to hold the largest market share and maintain its dominance throughout the forecast period. This is primarily due to the tricone design, which employs strong rolling cones with tungsten carbide inserts or cut teeth to provide reliable performance across a wide range of geothermal formations, interbedded hard/abrasive lithologies, fractured regions, and high-rock compressive strength, where drilling dynamics may occur quickly. Their known reliability under shock, vibration, and impact loading, and their high directional stability in adverse intervals, have made them a favorite among many operators seeking to reduce time lost to non-productive causes, including premature bit damage, incidents off-bottom, and frequent tripping. Moreover, ongoing innovation in bearing packages (sealed and high-load systems), gauge protection, and high-temperature metallurgy extends run life and reliability under high bottom-hole temperatures and aggressive hydraulics, supporting widespread use in both exploration and production well programs.

The Onshore Segment held the Largest Market Share in the Geothermal Drill Bits Market.

Based on application, the global geothermal drill bits market is segmented into Onshore and Offshore. In 2024, the Onshore segment is anticipated to hold the largest market share and maintain its dominance throughout the forecast period. This is mainly because most geothermal capacity additions and well-development initiatives are centered on terrestrial fields, where access to resources, permitting routes, and drilling logistics are relatively straightforward, and where project economics are more favorable than in the oceanic environment. The onshore geothermal drilling application has a wide variety of applications, with exploration, production, injection, making up wells to generate power and to heat a district, and with that, sustained repeated demand over time of drill bits able to withstand high temperatures, abrasive formations, and extended periods with a consistent rate of drilling and predictable bit life. Alongside this, the large-scale deployment of engineered geothermal designs (including EGS and closed-loop pilots) is increasingly occurring in onshore testbeds. It is also stimulating the need to design tricone and PDC tools with high mechanical specific energy for hard-rock operation.

North America Dominated the Global Geothermal Drill Bits Market

The North American region has the largest geothermal drill bit market in the world, and is likely to keep its lead throughout the forecast period. The first factor that can be considered to be pushing this leadership is the high density of geothermal project development and drilling capacity in the United States, backed by well-developed oil and gas services, long-standing experience in high-temperature drilling, and growing engineered geothermal (EGS) operations, and involvement of Canadians in clean-energy innovation and underground engineering. The focus on enhancing the economics of well drilling by shorter drilling cycles, longer bit life, and shorter non-productive time is among the primary reasons why the region will be a very attractive market in 2024, requiring high-performance PDC and tricone designs that are designed to work in hard-rock and abrasive formations and with high bottom-hole temperatures. Further, the supply chains, field trials in operation, and close cooperation between bit manufacturers, drilling contractors, directional drilling providers, and geothermal operators benefit the regional ecosystem by providing fast feedback loops on design optimization and reliability testing. As the policy and corporate decarbonization promise advances investment in the firm, low-carbon power, and direct-use heat, North America is in an excellent position to maintain a demand for advanced drill bit technologies that enhance the cost-per-meter and the smoothness in drilling various geothermal reservoirs.

U.S. held a dominant Share of the North America Geothermal Drill Bits Market in 2024

The United States market for geothermal drill bits is expected to continue expanding, driven by more geothermal projects in power and heating development that are currently in the planning stages and will soon enter the drilling phase. To improve resource availability and returns on projects, developers in the United States are drilling deeper wells into hotter, harder rock. This underscores the need for drill bits that can withstand longer, drill faster, and remain reliable even in high temperatures. The emphasis of buyers is on minimizing the overall cost per meter drilled, which makes them look at bits that minimize trips, minimize the damage that vibration can cause, and provide the same predictable performance in a variety of rock types. The U.S. drilling services base and the transfer of the hard-rock drilling expertise to oil and gas are also favorable to growth. Overall, the premium tricone, PDC, and hybrid bits should see increased demand.

Geothermal Drill Bits Industry Competitive Landscape

The global geothermal drill bits market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Geothermal Drill Bits Companies

Some of the major players in the market are Baker Hughes Company, SLB, Halliburton, NOV, Torquato Drilling Accessories Inc., Ulterra, Bit Brokers International, Varel Energy Solutions, Blast Hole Bit Company, LLC, and Apex Industries.

Recent Developments in the Geothermal Drill Bits Market

In October 2025, SLB, a global energy technology company and leading geothermal and renewable energy company, Ormat Technologies, announced an agreement to fast-track the development and commercialization of integrated geothermal assets, including enhanced geothermal systems (EGS). EGS is the next generation of geothermal technology, meant to unlock geothermal energy in regions beyond where conventional geothermal resources exist.

In July 2025, U.S. oilfield services firm Baker Hughes, opens new tab is collaborating with Controlled Thermal Resources in California to develop one of the world's largest single geothermal power projects, with plans to market the electricity to data centers. Baker Hughes joined Controlled Thermal Resources’ Hell’s Kitchen project near California’s Salton Sea, signing on for phase two, planned to deliver 500 MW of geothermal power, enough for about 375,000 homes, with potential to expand

Global Geothermal Drill Bits Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 6.28% |

Market size 2024 | USD 3,506.89 Million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | North America is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India |

Companies profiled | Baker Hughes Company, SLB, Halliburton, NOV, Torquato Drilling Accessories Inc., Ulterra, Bit Brokers International, Varel Energy Solutions, Blast Hole Bit Company, LLC, and Apex Industries |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Type, By Application, and By Region/Country |

Reasons to Buy the Geothermal Drill Bits Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The global geothermal drill bits market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Geothermal Drill Bits Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global geothermal drill bits market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the geothermal drill bits value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global geothermal drill bits market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including type, application, and regions within the global geothermal drill bits market.

The Main Objective of the Global Geothermal Drill Bits Market Study

The study identifies current and future trends in the global geothermal drill bits market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global geothermal drill bits market and its segments in terms of value (USD).

Geothermal Drill Bits Market Segmentation: Segments in the study include areas of type, application, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the geothermal drill bits industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the geothermal drill bits market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global geothermal drill bits current market size and its growth potential?

The global geothermal drill bits market was valued at USD 3,506.89 million in 2024 and is expected to grow at a CAGR of 6.28% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global geothermal drill bits market by Type?

The Tricone Drill Bits segment is expected to lead throughout the forecast period because its rolling-cone design with tungsten carbide inserts or milled teeth delivers reliable performance across variable geothermal formations, including hard and abrasive interbedded rocks, fractured zones, and high-strength lithologies where drilling conditions change quickly.

Q3: What are the driving factors for the growth of the global geothermal drill bits market?

• Expansion of Geothermal Power and District Heating Projects

• Need to Reduce Drilling Cost-Per-Meter through Higher ROP and Longer Bit Life

• Growth in Deep, High-Temperature, Hard-Rock Wells (Including EGS) Driving Premium Bit Demand

Q4: What are the emerging technologies and trends in the global geothermal drill bits market?

• Rising Adoption of PDC and Hybrid Bits

• Data-Driven Bit Optimization and Performance Monitoring

Q5: What are the key challenges in the global geothermal drill bits market?

• Harsh Downhole Conditions Accelerating Bit Wear

• Vibration Increasing Trips and NPT (Non-Productive Time)

Q6: Which region dominates the global geothermal drill bits market?

North America is expected to dominate the market, holding the largest share, driven by an active pipeline of onshore geothermal drilling programs in the United States, increasing engineered geothermal (EGS) initiatives, and a mature drilling services and manufacturing ecosystem.

Q7: Who are the key players in the global geothermal drill bits market?

Some of the key companies include:

• Baker Hughes Company

• SLB

• Halliburton

• NOV

• Torquato Drilling Accessories Inc.

• Ulterra

• Bit Brokers International

• Varel Energy Solutions

• Blast Hole Bit Company, LLC

• Apex Industries

Q8: How do drilling-cost reduction targets influence geothermal drill bit selection for municipal and utility-backed projects?

• Cost-Per-Meter Focus: Buyers prioritize bits that improve ROP and extend run length to lower total well cost.

• Reduced Trips and NPT: Longer bit life cuts tripping time and minimizes non-productive time from failures.

• Performance-Based Procurement: Tenders increasingly favor proven field results and cost-per-meter guarantees.

Q9: How do high-temperature operating conditions and hard-rock formations shape the adoption of premium geothermal drill bits?

• High-Temperature Reliability: Demand rises for cutters, bearings, and seals designed for elevated bottom-hole temperatures.

• Wear and Abrasion Resistance: Hard, abrasive lithologies drive the adoption of advanced materials and gauge protection.

• Vibration Management: Anti-whirl/anti-stick-slip designs gain preference to reduce damage and improve consistency.

Related Reports

Customers who bought this item also bought