- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Software-Defined Vehicle (SDV) Market: Current Analysis and Forecast (2025-2033)

Emphasis on SDV Type (Semi-SDV and SDV); E/E Architecture (Distributed, Domain Centralized, Zonal Control, and Hybrid/Mixed Propulsion Type); Vehicle Type (Passenger cars and Commercial vehicles); and Region/Country

Global Software-Defined Vehicle (SDV) Market Size & Forecast

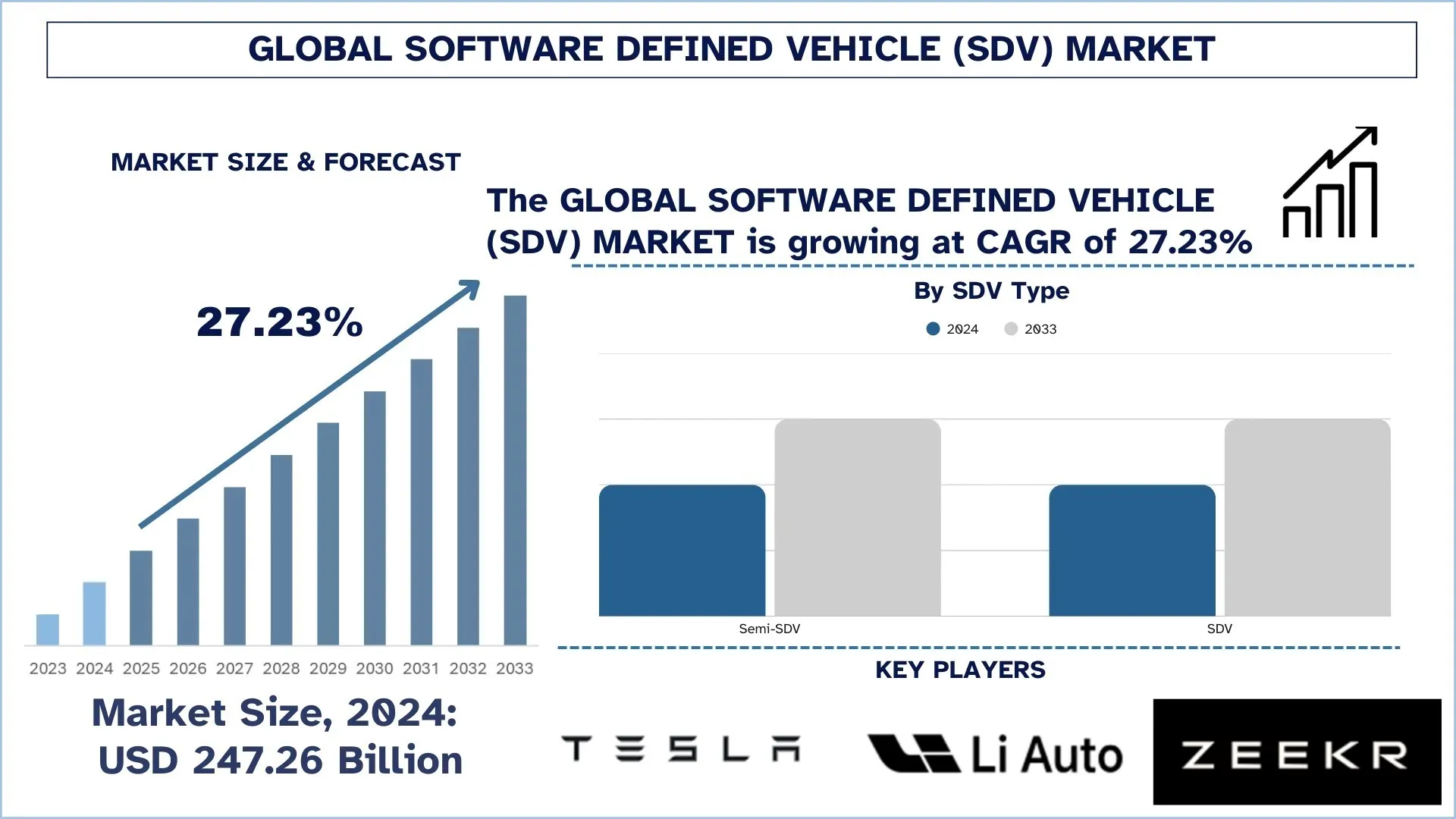

The Global Software-Defined Vehicle (SDV) Market was valued at USD 247.26 billion in 2024 and is expected to grow at a CAGR of around 27.23% during the forecast period (2025–2033F), driven by accelerating vehicle electrification, rising demand for connected and continuously upgradable features, and the increasing complexity of ADAS and digital cockpit systems across passenger and commercial vehicles.

Software-Defined Vehicle (SDV) Market Analysis

Automotive systems continue to become increasingly complex, and current practice requires a steady, reliable software functionality across a wide range of driving, connectivity, and lifecycle environments. Software-Defined Vehicle (SDV) offers businesses in the global market a growing trend, driven by increasing demand, advanced features, escalating cybersecurity risks, and shorter innovation cycles as electric and connected cars gain popularity. As the most significant solution for next-generation vehicle functionality, SDV platforms are perceived by OEMs and ecosystem partners as key to a differentiated user experience, shorter time-to-market, and long-term revenue from digital services. This is also supported by the substitution of fragmented ECU-heavy designs with centralized computing and zonal designs, which enhance scalability, reduce wiring complexity, and enable more efficient feature implementation across vehicle lines. Growing the market also requires a strategic combination of OTA updates, cloud-native development, middleware, and real-time data pipelines to monitor vehicle health, improve software quality, and enable the safe release of features. At the same time, the development of advanced ADAS and early autonomous functionality in the previous year has placed strain on SDV stacks that must operate in harmony with safety-critical systems, functional safety, and cybersecurity standards, thereby changing vehicle architectures to be smarter, more responsive, and future-oriented.

Global Software-Defined Vehicle (SDV) Market Trends

This section discusses the key market trends that are influencing the various segments of the global Software-Defined Vehicle (SDV) market, as found by our team of research experts.

Centralized Compute + Zonal E/E Architecture Rollout

One of the most evident trends shaping the global Software-Defined Vehicle (SDV) market is the industry-wide transition to centralized high-performance computing (HPC) and software-centric E/E architectures. With increasingly compute-intensive vehicles, particularly advanced ADAS, rich digital cockpits, and data-driven services, OEMs are migrating dozens of function-specific controllers to lower counts of more powerful compute nodes capable of running many applications, standardizing software deployment as well as scaling features across platforms. The pace of this trend is accelerating as centralized computing enables software reuse across vehicle lines, consistent cybersecurity controls, and lifecycle improvements through controlled software releases rather than hardware modifications. It also facilitates more responsive development practices, which allow the integration of new capabilities faster, better diagnostics, and continuous quality improvements after sale. As a vivid example of this trend, the Adaptive Platform design document of AUTOSAR observes that future car functionality like highly automated driving implements highly complex software requiring the use of computing resources and meeting the toughness of the integrity and security demands, and that software must evolve throughout the life of the vehicle driving the necessity of a platform that delivers high-performance computing and supports over-the-air updates.

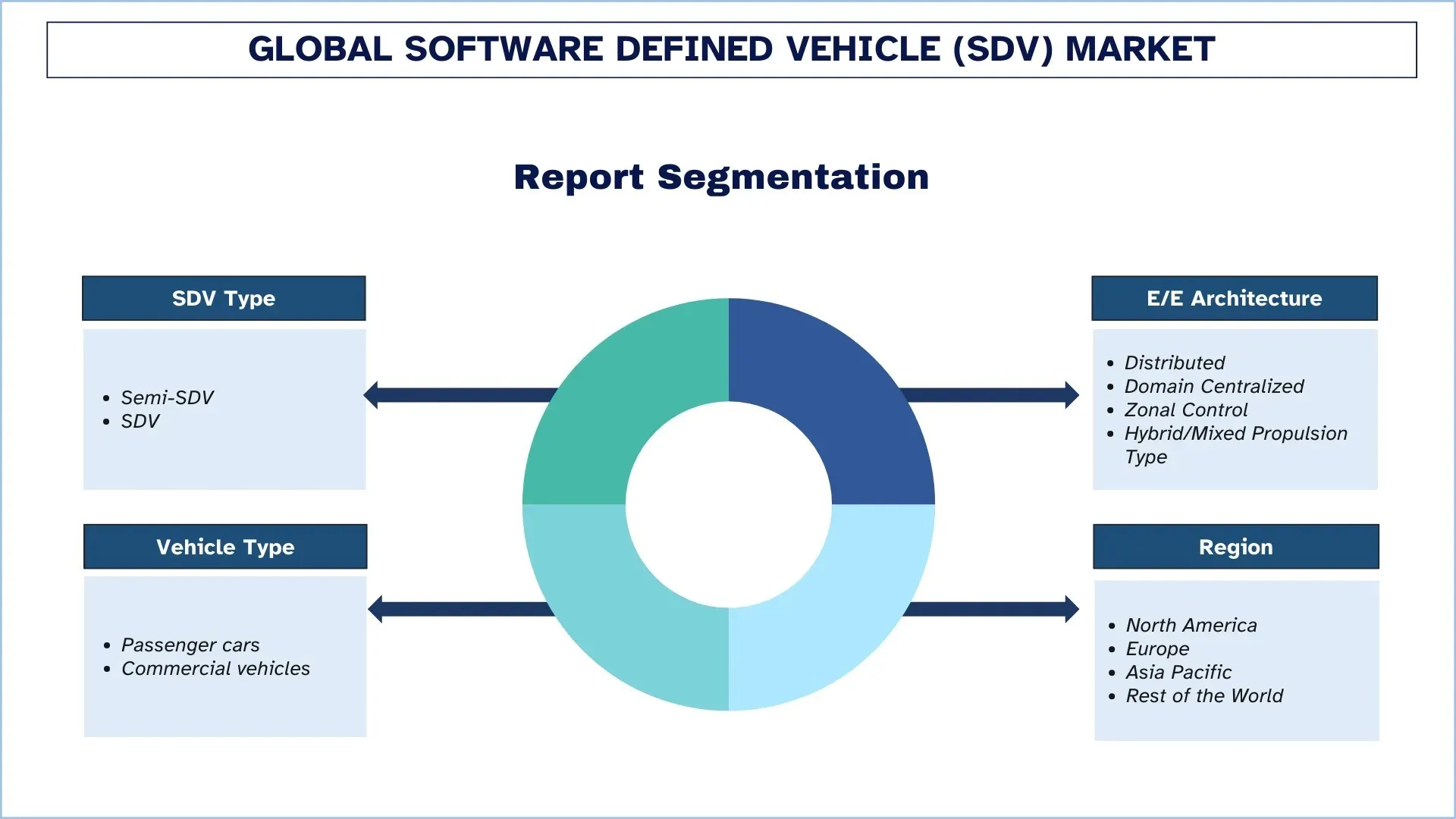

Software-Defined Vehicle (SDV) Industry Segmentation

This section provides an analysis of the key trends in each segment of the global Software-Defined Vehicle (SDV) market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Semi-SDV Segment Dominates the Software-Defined Vehicle (SDV) Market

Based on SDV type, the global Software-Defined Vehicle (SDV) market is segmented into Semi-SDV and SDV. In 2024, the Semi-SDV segment is anticipated to hold the largest market share and continue its dominance throughout the forecast period. This is mainly because most OEMs are currently in a transition phase, integrating traditional distributed ECU architectures with selective software-defined features, including OTA updates, feature-on-demand, connected services, and domain-level controllers. These cars provide immediate functionality through faster feature rollout, diagnostics, and user experience, without necessitating a complete redesign to centralized computing and zonal designs, and are the most realistic and scalable for high-volume programs. The SDV segment will, however, experience the fastest growth rate due to accelerating electrification, increasing complexity of ADAS, and OEMs' strategy to develop unified vehicle operating systems and centralized compute platforms. To support rapid software development cycles, cross-model feature reuse, ongoing cybersecurity patches, and sustained digital revenue, automakers are considering full SDV stacks, at the cost of increased hardware complexity and enhanced lifecycle performance by ensuring that the vehicle architecture is software-first.

The Distributed Segment held the Largest Market Share in the Software-Defined Vehicle (SDV) Market.

Based on E/E architecture, the global Software-Defined Vehicle (SDV) market is segmented into Distributed, Domain Centralized, Zonal Control, and Hybrid/Mixed architectures. In 2024, the Distributed segment is anticipated to hold the largest market share and continue its dominance throughout the forecast period. This is largely because most vehicles on the road and in current production are based on legacy, ECU-intensive distributed networks, where function additions are incremental, OEMs are cost-constrained, and reuse platforms and familiar supply chains prevail. These architectures enable early SDV functions, including rudimentary connectivity, diagnostics, and partial OTA updates, without necessitating a complete redesign of the vehicle; therefore, they are the most widespread baseline across high-volume models. The Zonal Control segment, however, will grow at the fastest rate owing to OEM migration to centralized computing, lower wiring-harness complexity, and the need to scale software characteristics across vehicle lines efficiently. Zonal architectures enable more effective hardware and software partitioning, faster feature delivery, enhanced cybersecurity operations, and support for more advanced ADAS loads, making automakers smarter, more scalable, and truly software-first vehicle platforms.

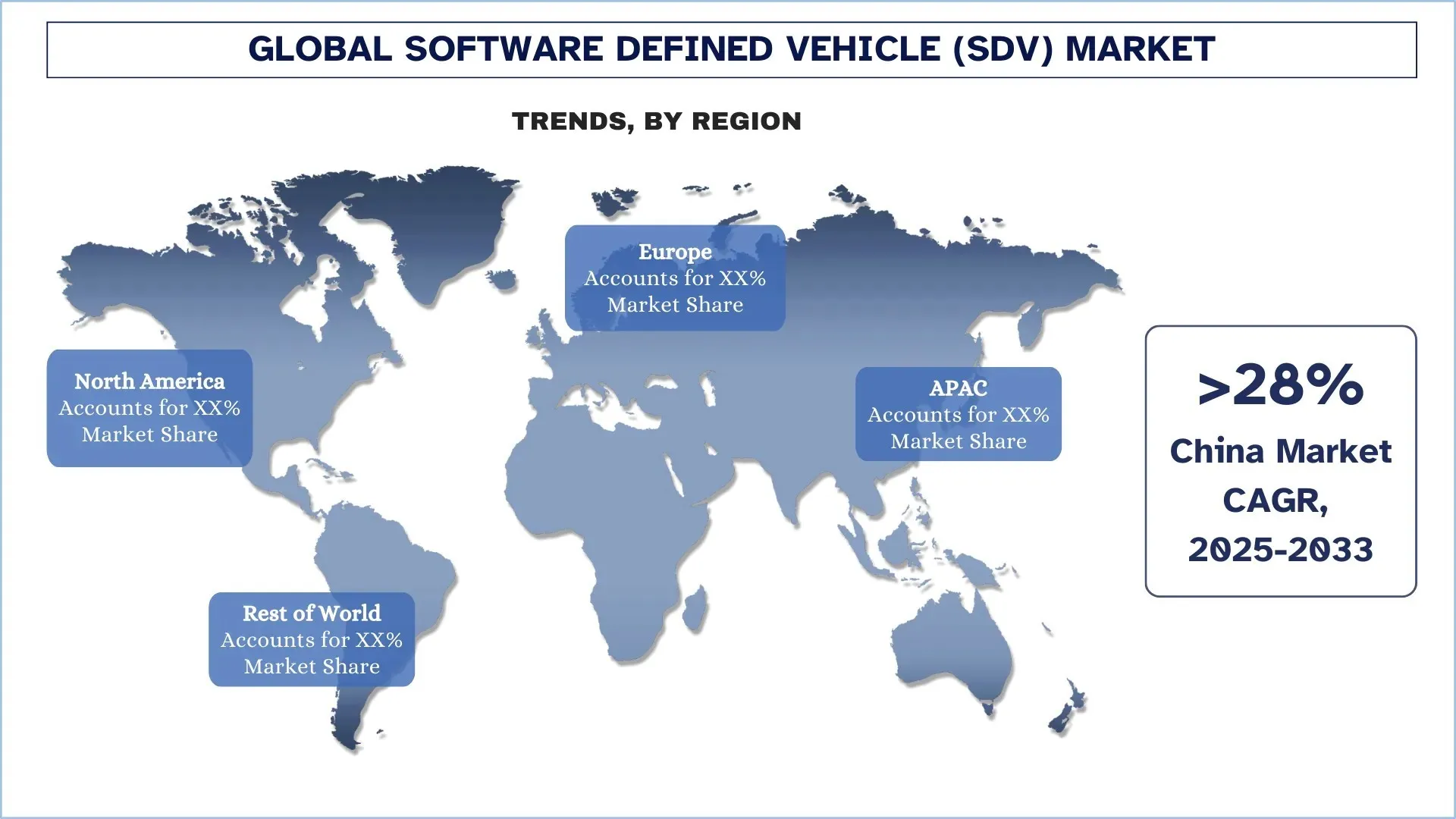

Asia Pacific Dominated the Global Software-Defined Vehicle (SDV) Market

The Asia-Pacific region has enjoyed a lead in the global SDV market, supported by strong bases in vehicle manufacturing and electronics supply chains, especially in China, Japan, and India. Some of the world's largest OEMs, semiconductor and component companies, and high-volume EV manufacturers are located here, generating significant interest in connected platforms, OTA-capable architectures, and centralized computing to differentiate vehicles and shorten innovation cycles. As vehicle production scales, especially for electric and connected models, advanced E/E architectures, software platforms, and integrated vehicle operating systems are also increasing. The surge in urbanization and the adoption of digital technologies in emerging markets are accelerating demand for connected services, smart cockpits, and safety improvements. Additionally, the development of more sophisticated ADAS capabilities and cybersecurity requirements is driven by the region's focus on enhancing safety, user experience, and lifecycle updates. With the growing penetration of EVs, digital offerings, and platform-based product approaches, the Asia-Pacific region is leading in SDV deployments.

China held a dominant Share of the Asia Pacific Software-Defined Vehicle (SDV) Market in 2024

China's dominance in the Software-Defined Vehicle (SDV) market is primarily attributable to its large-scale automotive production and rapid adoption of next-generation digital vehicle technologies. The country has a large base of OEMs, Tier-1 suppliers, and technology ecosystem players, which is accelerating demand for SDV stacks in passenger and commercial programs. This is further reinforced by China's strong momentum in electric and connected vehicles, in which OTA updates, intelligent cockpits, and software-enabled ADAS features have become key differentiators, prompting automakers to invest in centralized computing, domain/zonal E/E architectures, and scalable middleware.

Software-Defined Vehicle (SDV) Industry Competitive Landscape

The global Software-Defined Vehicle (SDV) market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Software-Defined Vehicle (SDV) Companies

Some of the major players in the market are Tesla, Li Auto Inc., ZEEKR, XPENG INC., NIO, Rivian, The Ford Motor Company, General Motors, Volkswagen Group, and Valeo.

Recent Developments in the Software-Defined Vehicle (SDV) Market

- In January 2025, XPENG announced the global release of the XOS 5.4 OTA update, enhancing intelligent driving, safety, and personalization. Features include AI Guard for safety, Smart Speed Limit Recognition, expanded voice control in multiple languages, and Personalized Operating System 2.0.

- In January 2025, Hyundai Motor Group partnered with NVIDIA at CES 2025 to integrate AI, digital twins, and generative AI into next-gen mobility and manufacturing systems. The collaboration will optimize autonomous driving, enhance vehicle design, and improve factory efficiency using NVIDIA's advanced simulation and AI technologies.

Global Software-Defined Vehicle (SDV) Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 27.23% |

Market size 2024 | USD 247.26 Billion |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | Asia Pacific is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India |

Companies profiled | Tesla, Li Auto Inc., ZEEKR, XPENG INC., NIO, Rivian, The Ford Motor Company, General Motors, Volkswagen Group, and Valeo |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By SDV Type; By E/E Architecture, By Vehicle Type, and By Region/Country |

Reasons to Buy the Software-Defined Vehicle (SDV) Market Report:

- The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

- The report briefly reviews overall industry performance at a glance.

- The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

- Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

- The study comprehensively covers the market across different segments.

- Deep dive regional-level analysis of the industry.

Customization Options:

The global Software-Defined Vehicle (SDV) Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Software-Defined Vehicle (SDV) Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global Software-Defined Vehicle (SDV) market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the Software-Defined Vehicle (SDV) value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global Software-Defined Vehicle (SDV) market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including SDV type, E/E architecture, vehicle type, and regions within the global Software-Defined Vehicle (SDV) market.

The Main Objective of the Global Software-Defined Vehicle (SDV) Market Study

The study identifies current and future trends in the global Software-Defined Vehicle (SDV) market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global Software-Defined Vehicle (SDV) market and its segments in terms of value (USD).

Software-Defined Vehicle (SDV) Market Segmentation: Segments in the study include areas of SDV type, E/E architecture, vehicle type, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the Software-Defined Vehicle (SDV) industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the Software-Defined Vehicle (SDV) market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global Software-Defined Vehicle (SDV) current market size and its growth potential?

The global Software-Defined Vehicle (SDV) market was valued at USD 247.26 billion in 2024 and is expected to grow at a CAGR of 27.23% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global Software-Defined Vehicle (SDV) market by SDV Type?

The Semi-SDV segment is anticipated to hold the largest market because most OEMs are currently in a transition phase, integrating traditional distributed ECU architectures with selective software-defined features, OTA updates, feature-on-demand, connected services, and domain-level controllers.

Q3: What are the driving factors for the growth of the global Software-Defined Vehicle (SDV) market?

• Rising demand for connected, upgradable vehicles

• ADAS complexity and compute needs

• OEM shift to lifecycle revenue models

Q4: What are the emerging technologies and trends in the global Software-Defined Vehicle (SDV) market?

• Centralized compute + zonal E/E architecture rollout

• Vehicle OS and middleware standardization

Q5: What are the key challenges in the global Software-Defined Vehicle (SDV) market?

• Legacy architecture migration

• Software talent and delivery maturity gaps

Q6: Which region dominates the global Software-Defined Vehicle (SDV) market?

The Asia-Pacific region has enjoyed a lead in the global SDV market, supported by strong bases in vehicle manufacturing and electronics supply chains, especially in China, Japan, and India.

Q7: Who are the key players in the global Software-Defined Vehicle (SDV) market?

Some of the key companies include:

• Tesla

• Li Auto Inc.

• ZEEKR

• XPENG INC.

• NIO

• Rivian

• The Ford Motor Company

• General Motors

• Volkswagen Group

• Valeo

Q8: How does the rising adoption of electric and connected vehicles influence the growth of the Software-Defined Vehicle (SDV) market?

• OTA-First Feature Expectations: EVs and connected cars rely on frequent software updates for feature upgrades, bug fixes, and performance optimization, accelerating demand for SDV stacks.

• Centralized Compute Need: Higher software content and ADAS workloads increase the need for centralized computing and scalable middleware to manage vehicle functions efficiently.

• Lifecycle Value Creation: OEMs use SDV capabilities to enable feature-on-demand, remote diagnostics, and continuous improvements, creating long-term digital revenue opportunities.

Q9: How do cybersecurity and software update regulations shape the development and adoption of SDVs globally?

• Software Update Compliance: Regulations such as UN R156 raise requirements for software update management, pushing OEMs to implement robust OTA governance and traceability.

• Cybersecurity Mandates: Frameworks like UN R155 increase focus on secure-by-design development, vulnerability management, and secure update pipelines across the vehicle lifecycle.

• Functional Safety Alignment: Safety-critical software and ADAS features require stricter validation and controlled releases, shaping SDV platform architecture and tooling.

Related Reports

Customers who bought this item also bought

Freight Railcar Repair Market: Current Analysis and Forecast (2025-2033)

Emphasis on Repair Type (Mechanical (Brake System, Coupler & Draft Gears, Bearing & Axles, Wheels & Wheelsets, Doors & hatches, Pneumatic Systems, Others), Structural (Boday & Frame Repair, Welding & Metalworks, Corrosion Prevention & Repair, Roof, sides & Underbody Repair, Others), Interior (Flooring & Subflooring, Interior Lining & Insulation, Others)); By Service (Mobile, On-Site); and Region/Country

May 9, 2025

Automotive Sprocket Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Timing Sprockets, Roller Chain Sprockets, Silent Chain Sprockets, and Others); Vehicle Type (Two-Wheelers, Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Electric Vehicles (EVs) & Hybrid Vehicles); Sales Channel (Aftermarket and Original Equipment Manufacturer (OEM)); and Region/Country

May 6, 2025